Report Board

Sivers / SIVEF: A Laser-Source Bottleneck Candidate in AI Photonics

Sivers is not a full optical-module vendor. Its edge is upstream high-power DFB/CW laser arrays plus mmWave beamforming. The AI photonics bottleneck is real, but production proof, restated accounts, and valuation are the key checks.

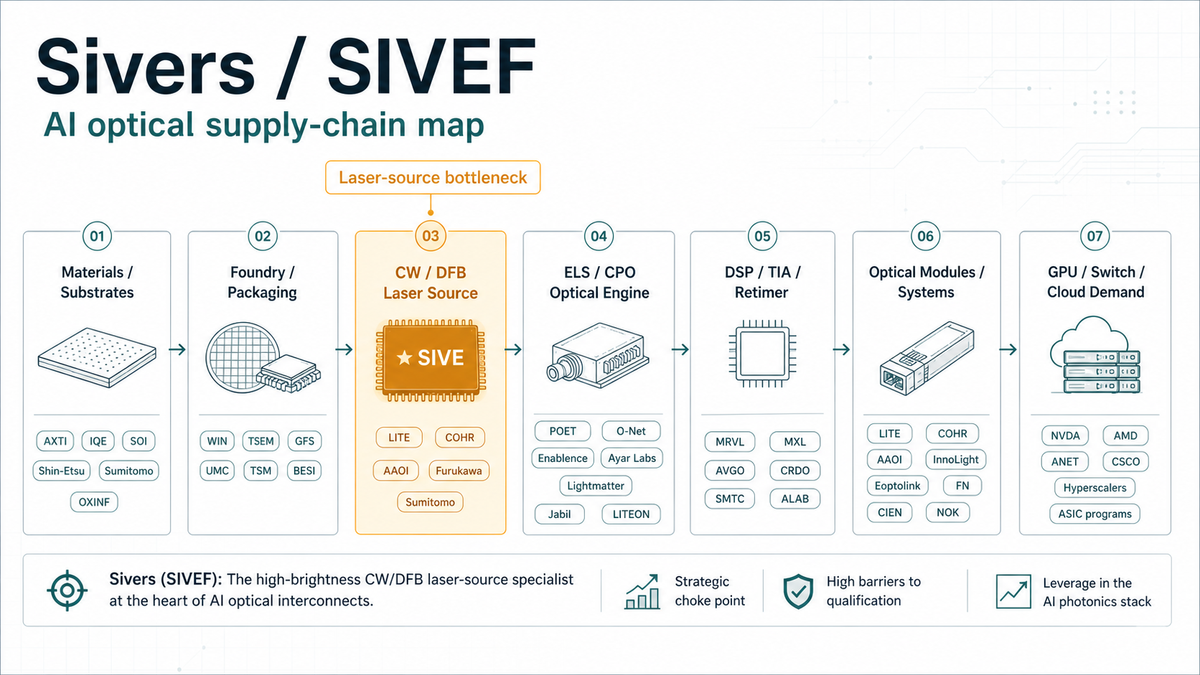

AI Optical Supply-Chain Position Map

A layer-by-layer map of the CPO-related companies repeatedly discussed in the Serenity/X market map; Sivers/SIVE is highlighted in the upstream CW/DFB laser-source layer.

Materials / substrates

InP, GaAs, SOI, and optical materials define upstream elasticity. Serenity's photonics basket often places AXTI, IQE, and SOI in this materials/substrate layer.

Wafer / foundry / packaging

This layer turns III-V laser and silicon-photonics designs into manufacturable parts. Sivers' WIN partnership is the bridge from samples to multi-customer supply.

Laser-source chokepoint

This is the highlighted Sivers slot. Serenity groups SIVE with the CPO/CW laser chokepoint; official evidence comes from DFB arrays, Jabil 1.6T, O-Net/Enablence ELS, POET, and WIN.

ELS / CPO engines

This layer combines light sources, silicon photonics, packaging, and module design. Sivers is not the full engine vendor, but its DFB/CW laser content can enter the BOM.

DSP / TIA / retimers

PAM4 DSPs, TIAs, retimers, and CXL/PCIe connectivity chips control the electrical-to-optical signal chain. They are parallel bottlenecks, not substitutes for lasers.

Optical modules / systems

Module and network-system vendors convert qualification, capacity, and integration into more visible revenue. Sivers remains the upstream component inside that stack.

GPU / switches / cloud demand

Final demand comes from AI scale-up and scale-out networks. NVIDIA, AMD, custom ASIC programs, and cloud buildouts determine how long upstream laser scarcity lasts.

A Reviewable Logic Chain

Each card stays open and maps one transmission node without collapsible controls or pseudo-precise scores.

InP / foundry / packaging

Before Sivers sit InP epitaxy, wafer manufacturing, packaging, and yield. The WIN partnership is about turning Sivers' DFB design into scalable manufacturing.

DFB / CW laser arrays

The core position: high-power, narrow-linewidth, wavelength-stable light sources for silicon photonics, ELS, CPO, 1.6T pluggables, and LiDAR.

ELS / CPO / 1.6T modules

O-Net/Enablence integrate ELS modules, POET integrates optical-interposer light engines, and Jabil works on 1.6T LRO modules. Sivers supplies the light source.

AI datacenter / HPC / LiDAR

Demand comes from scale-up and scale-out networks, CPO, pluggables, and LiDAR. The production proof window is 2026 qualification into 2027 customer plans.

SATCOM / FWA / Defense

Wireless supplies mmWave RFICs, beamformers, and antenna modules into ALL.SPACE, Tachyon, Doosan, NEMC/BAE/MIT Lincoln/Columbia, and defense programs.

Investment Question: Where Does Sivers Actually Sit?

Sivers Semiconductors is easy to label as AI photonics, CPO, 1.6T, SATCOM, or defense. The cleaner first-principles view is narrower: it is not a GPU vendor, switch ASIC vendor, full optical-module vendor, or hyperscaler network architect. It combines two enabling component layers: high-power DFB/CW laser arrays in Photonics and mmWave RFIC/beamforming technology in Wireless.

The bottleneck answer is therefore layered. Photonics has real bottleneck potential because 800G to 1.6T/3.2T optical networking raises the bar for laser power, wavelength stability, reliability, thermal management, and scalable manufacturing. Wireless is a real second growth line across SATCOM, FWA, and defense, but it is not the same AI data-center bottleneck.

Serenity's Market Map: SIVE in the Laser Chokepoint Layer

The useful part of Serenity's X framework is that it is not a single-ticker view. It splits CPO and AI photonics into materials, foundry/manufacturing, laser sources, ELS/CPO optical engines, DSP/TIA, modules, and end cloud demand. In that framework, SIVE, LITE, COHR, AAOI, and MTSI sit near the CW/EML laser chokepoint; WIN, TSEM, and GFS sit in manufacturing; AEHR, SOI, AXTI, and IQE sit closer to testing and materials.

I treat that as a market-map reference, not an official source of company facts. The official evidence still comes from Sivers' annual report and releases: DFB laser arrays, the WIN production partnership, Jabil 1.6T LRO, O-Net/Enablence external light source work, POET light-engine work, and Wireless-side NEMC/Tachyon/ALL.SPACE validation. The infographic highlights SIVE because it lands in the upstream laser-source bottleneck layer.

Core Competence: Laser Performance Plus a Scalable Manufacturing Path

The core asset in Sivers Photonics is the DFB laser-array platform. CPO and silicon photonics do not remove the need for III-V light generation; they make external light sources, coupling, thermal stability, and reliability more central. Sivers' annual report frames DWDM laser arrays coupled with co-packaged silicon photonics chiplets as strategically important for AI data-center networks.

That is where Sivers looks most like a bottleneck candidate. It does not control the whole module, but the light source is a physical layer that cannot be replaced by plain CMOS. External light sources matter because they move temperature-sensitive lasers away from high-heat processor packages, improving wavelength stability and serviceability.

Supply-Chain Position: Upstream Enabler, Not System Owner

In the AI optical-interconnect chain, Sivers sits between compound-semiconductor manufacturing and module/system integration. Upstream sit InP epitaxy, wafer manufacturing, packaging, and yield. Sivers supplies DFB/CW laser arrays. Downstream sit O-Net/Enablence ELS integration, POET optical-interposer light engines, Jabil 1.6T LRO modules, and ultimately switches, NICs, GPU clusters, and hyperscalers.

That is a strong position, but it is not full control. Pricing power can be shared or taken by module vendors, hyperscalers, qualification cycles, packaging yield, and alternative laser suppliers. The key proof is whether Sivers moves from sampling and development partnerships into multi-customer production plans.

Why Photonics Is the Bottleneck Candidate and Wireless Is the Option

Photonics is driven by a physical constraint. AI scale-up and scale-out networks are forcing more data movement from electrical links into optical links. 1.6T, 3.2T, CPO, and ELS all point to the same problem: more bandwidth in shorter, denser, hotter systems without exploding power consumption. Sivers' light source sits near the front of that problem.

Wireless is different. Sivers Wireless has genuine value in SATCOM, FWA, FR3 5G/6G, and defense. The NEMC Year 2 award, Tachyon 60 GHz partnership, Doosan Ka-band work, and ALL.SPACE progress all matter. But these are engineering and productization paths, not the same scarcity premium as AI optical light sources.

The Main Counter-Evidence: Small Revenue, Losses, and Restated Accounts

The better the technology story, the more the financial proof matters. Sivers' 2025 Annual Report restated full-year net sales to SEK 306.6M, EBIT to SEK -177.8M, and net loss to SEK -222.6M. The company is also upgrading 2024 and 2025 reporting toward PCAOB standards for a potential Nasdaq New York dual listing and postponed Q1 2026 reporting to May 29, 2026.

That is not automatically negative, but it changes the burden of proof. On the May 19 delayed quote snapshot, SIVE.ST was around SEK 48.8 and MarketScreener showed market cap near SEK 14.21B, with the shares up more than 1000% year to date. The market has already paid for a large part of the AI photonics option.

Conclusion: A Light-Source Bottleneck Candidate, Not Yet a Proven Leader

My conclusion: Sivers is a high-quality candidate in the AI optical-interconnect bottleneck chain, but not yet a proven module-scale leader. The core competence is high-power DFB/CW laser arrays plus a scalable manufacturing route. The supply-chain position is upstream light-source and ELS enablement. The proof window is the transition from 2026 samples and qualifications into 2027 production revenue.

If Jabil, POET, O-Net/Enablence, or other module customers produce quantified production orders, the Photonics thesis can shift from theme exposure to component ramp. If the partnerships stay at development and demo stage while cash burn and dilution continue, the current bottleneck premium can compress back toward a small R&D component-company valuation.

Sivers' supply-chain position, bottleneck strength, and proof gates

Static research snapshot as of 2026-05-20, not investment advice. SIVEF is the U.S. OTC/Pink quote; primary liquidity and company disclosures remain tied to Nasdaq Stockholm SIVE.ST and official Sivers releases.

| Position | Verified facts | Ticker / chain | Next revenue bridge | Bottleneck read | Risk / disproof |

|---|---|---|---|---|---|

| Photonics: high-power DFB/CW laser arrays | Sivers' annual report frames AI datacenter/HPC optical interconnects as the Photonics focus and flags possible CW laser shortages in the 800G to 1.6T/3.2T transition. | SIVEF / SIVE.ST | Jabil 1.6T LRO, O-Net/Enablence ELS, POET light engine, and the Q4 2026 LiDAR ramp are the key revenue bridges. | Bottleneck: high | The edge is light-source performance, reliability, wavelength stability, and scalable process capability. Sivers is not the full CPO or module owner. |

| Manufacturing scale: WIN outsourced production | The March 2025 WIN partnership is intended to scale high-power DFB laser and array production for CWDM/DWDM applications. | WIN + Sivers | The 2027 proof is yield, cost, delivery cadence, and multi-customer production plans after qualification. | Bottleneck precondition | The bottleneck is not just design. Without scalable manufacturing, Sivers remains a sampling and NRE story. |

| CPO/ELS: O-Net + Enablence + POET | O-Net/Enablence/Sivers are developing an 8-channel ELS module, while POET pairs Sivers DFB lasers with its Optical Interposer. | CPO ecosystem | H1 2026 prototypes, year-end 2026 production readiness, and 2027 production plans are the proof path. | Bottleneck: medium-high | ELS is crucial to CPO because it removes temperature-sensitive lasers from hot processor packages, but alternative laser and integration paths remain. |

| 1.6T pluggable: Jabil LRO | Jabil plans to use Sivers DFB lasers in a 1.6T linear receive optical transceiver for AI data centers. | Jabil module path | Watch module qualification, customer design-ins, production timing, and laser content per module. | Bottleneck: medium | Sivers can capture light-source BOM, while module and customer pricing power may sit elsewhere. |

| LiDAR: narrow-linewidth high-power lasers | Q4 2025 disclosures pointed to a lead LiDAR customer ramping in Q4 2026, with possible cumulative 2026-2030 revenue of $28M-$53M. | Photonics non-DC | If automotive and industrial LiDAR scale after 2027, it can become a second Photonics revenue pillar. | Bottleneck: medium | LiDAR proves technology reuse, but customer concentration and market timing need separate tracking. |

| Wireless: mmWave RFIC / beamformer / modules | Wireless has validation across ALL.SPACE TRL6, Doosan Ka-band, Tachyon 28/60 GHz, and NEMC EW STAR. | SATCOM / FWA / Defense | $6.6M NEMC Year 2, $1.5M Tachyon 60 GHz, $3M Tachyon 28 GHz production PO, and defense-prime contracts. | Bottleneck: medium | Valuable second line and government-funded validation, but not the same AI datacenter scarcity layer. |

| Financial/valuation: proof needed after re-rating | Restated 2025 net sales were SEK 306.6M, EBIT was SEK -177.8M, and net loss was SEK -222.6M. Q1 2026 was postponed to May 29. | Risk ledger | On the May 19 delayed quote snapshot, SIVE.ST was about SEK 48.8 and MarketScreener showed market cap near SEK 14.21B, after a year-to-date move above 1000%. | Valuation risk: high | A strong technology position does not automatically mean the price is cheap. Production revenue, gross margin, cash runway, and dilution must reset the view. |

Sivers Semiconductors · SIVE.ST / PINK:SIVEF · 2026-05-20 snapshot

Earnings releases, announcements, filings, estimate tables, and reviewable sources.

- Core signal

- High-power DFB/CW laser arrays, ELS/CPO partnerships, WIN manufacturing scale-up, Jabil 1.6T LRO, POET/O-Net/Enablence, NEMC defense funding, 2025 restated financials

- Current read

- The supply-chain position is strong, but Sivers does not control the full system. It is an upstream enabling component vendor: laser sources and ELS enablement in optical interconnects, RFIC/beamforming in SATCOM, FWA, and defense. The next proof is conversion of 2026 samples and qualifications into 2027 production revenue.

- Next question

- Is SIVEF's edge real technology scarcity, customer validation, or a market that has already capitalized the CPO/AI optics story?

Sivers' edge is high-power DFB/CW laser arrays plus mmWave beamforming, not full optical-module ownership.

Photonics has real AI optical-interconnect bottleneck potential because ELS/CPO/1.6T raise requirements for light-source stability, power, and scalable production.

The WIN partnership is critical: without manufacturing scale, the technology remains a sampling story.

Wireless is a valuable second line across SATCOM, FWA, and defense, but not the same scarcity layer as AI datacenter optics.

The stock already reflects a lot of good news; 2025 restatements, Q1 delay, cash flow, and dilution must stay central to the risk ledger.

May 29, 2026 Q1 report: revenue, cash, gross margin, restatement impact, and Q2/Q3 language.

Jabil 1.6T LRO qualification, customer design-ins, production timing, and Sivers laser content per module.

POET / O-Net / Enablence ELS and CPO prototypes in H1 2026 and production-readiness language by year end.

WIN manufacturing disclosures: yield, capacity, cost, or multi-customer production plans.

Lead LiDAR customer Q4 2026 ramp and the shape of 2027 revenue contribution.

Wireless conversion from NEMC, Tachyon, ALL.SPACE, and Doosan development awards into product revenue.

Potential Nasdaq New York dual listing, financing, warrant/option dilution, and cash runway.